Abstract under adverse circumstances facing overseas "dual", Suntech bankruptcy, in 2014 China's polysilicon output reached 132,000 tons, an increase of 57%; wafer production reached 38GW, up 28%; solar cells production reached 33GW, a year-on-year increase...

In the face of the overseas "double opposition" and Wuxi Suntech bankruptcy, China's polysilicon production in 2014 still reached 132,000 tons, an increase of 57%; wafer production reached 38GW, an increase of 28%; battery production reached 33GW , a year-on-year increase of 32%; component production reached 35GW, an increase of 27.2%. As the world's largest PV market, China's PV industry chain has gradually changed from the middle to the downstream, and all the enterprises in China's PV industry chain have entered the top ten in the world, such as 4 polysilicon, 8 silicon wafers, 5-6 solar cells, and 5 components. ~6, and the first place is a Chinese company. In 2014, China's polysilicon production accounted for 43% of the world's total, silicon wafers accounted for 76% of the world, battery segments accounted for about 59%, and components accounted for about 75%. After China's photovoltaic industry has experienced a slow-fast-explosion-stagnation-rising development process, the photovoltaic industry has fallen into the trap of “low-end industrial value chainâ€. Promoting the technological innovation of China's photovoltaic enterprises has become an important way to break through the low-end locking and embedded in the high-end of the global value chain. Many domestic scholars have carried out preliminary research on the status quo and improvement path of China's PV industry's international competitiveness. Wang Wenxiang et al. discussed and analyzed the formation of China's PV industry's dilemma and its development path. Lan Xiaoping analyzed the development status of China's PV industry and its prospects. Looking forward to it; Liao Mei et al. used the GTAP model to analyze the export effects of government subsidies in China's photovoltaic industry.

The above research is based on the vertical analysis of the domestic PV industry chain and its development status, and lacks analysis of the industrial chain of other countries in the world. This paper will use the combination of principal component analysis, factor analysis and cluster analysis to The external photovoltaic industry chain conducts research and analysis, draws conclusions and provides guiding suggestions for the development of China's photovoltaic industry.

1 Static analysis of the competitiveness of photovoltaic industry

Based on the comprehensive evaluation and analysis of the competitiveness of the photovoltaic market based on the industrial chain, the existing relevant literature mainly uses Porter “diamond model†and analytic hierarchy process to analyze and analyze the global PV industry chain from a macro perspective. The photovoltaic industry chain design is a relatively systematic and comprehensive evaluation index system. This paper will use the combination of factor analysis, cluster analysis and principal component analysis. Mainly based on the following considerations: First, the evaluation of the early evaluation of the "diamond model" has a certain analytical value. The principal component analysis method and the factor analysis method can make the evaluation more objective and scientific from the perspective of data; Cluster analysis based on factor analysis can subdivide the national PV industry chain at a scientific level, so that the analysis results can be deeper.

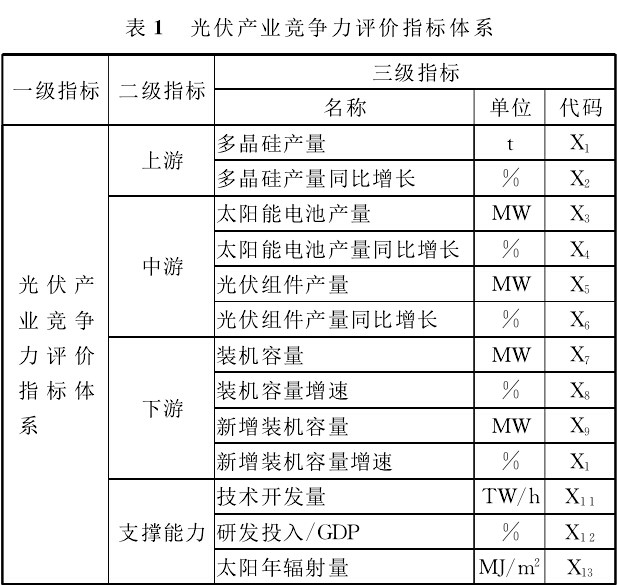

The research in this paper attempts to construct a systematic, hierarchical and scientific evaluation index system. The photovoltaic industry chain includes six parts: silicon material, ingot (pull rod), slice, battery, battery assembly, and application system. The upstream is the silicon raw material, silicon wafer and other links. The middle reaches are the battery, photovoltaic components and other links. The downstream is the installation of photovoltaics, application systems and other links. From a global perspective, the number of companies involved in the six links of the industry chain has increased substantially.

Today, China's PV market industry chain presents a pyramid-shaped model, that is, the bottom is big and small, there are few enterprises engaged in upstream manufacturing and refining, and there are many industries engaged in mid-stream PV modules and solar cell manufacturing, and most of them are engaged in downstream PV system applications. . China's photovoltaic industry started late, and currently focuses on the low-end production links of the photovoltaic industry chain, mainly in the low-tech sectors. In the international market, it has always played the role of a major manufacturing country, but lacks core technology and weak international competitiveness.

1.1 Establishment of indicator system

This paper takes the evaluation target, namely the global photovoltaic industry chain competitiveness evaluation as the first-level indicator, and takes the upstream, midstream, downstream and supporting capacity of the industrial chain as the secondary indicators, respectively, selecting the United States, Germany, China, Japan, Britain, France, Italy, South Korea. Ten countries in Australia and Spain were selected as evaluation targets. It is based on the analysis of the data of ten countries to compare the stages of the industrial chain in which ten countries are located. From the overall perspective, judge the stage of China's PV industry at the international level, and use factor analysis to analyze and evaluate the indicators. The industrial chain conducts competitiveness evaluation and proposes a path improvement plan for the development of China's photovoltaic industry. The specific indicators are established as shown in Table 1.

1.2 Factor analysis

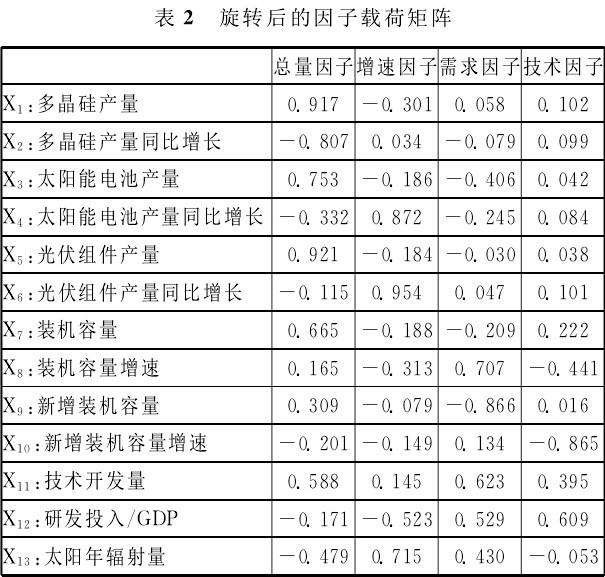

Taking the data of 2013 as an example, the comparative analysis of the competitiveness level of the global PV industry chain is carried out. Applicability test on the data, using the SPSS21.0 software, the KMO value is calculated to be 0.701>0.7, and the P value corresponding to the Bartlett star test statistic is 0.00<0.05, indicating that the satisfaction is satisfied. Prerequisites for factor analysis. According to the principle of factor analysis, the correlation coefficient matrix is ​​established, and the cumulative variance contribution rate of the first four factors is 84.642%, which can represent most of the information of the original data. Therefore, four factors are extracted for analysis. In order to make the extracted factors more naming and interpretable, the maximum variance method is used to perform the factor rotation, and the structure of the factor load matrix is ​​simplified. The rotated factor load matrix is ​​shown in Table 2.

The regression method is used to calculate the matrix of factor score coefficients, and then the scores of each factor are obtained. Using the scores of each factor, using the variance contribution rate as the weight, calculate the factor comprehensive score and sort it. The calculation formula is as follows. The result is Table 3:

F comprehensive = 0.326F1 + 0.215F2 + 0.185F3 + 0.12F4

From the perspective of various public factors, from the perspective of aggregate factors, the rankings are basically consistent with the comprehensive rankings, which can reflect the competitiveness of various countries' industrial chains. China, Germany, and the United States rank high. In 2013, China's polysilicon production, battery production, and installed capacity. The capacity ranks first in the world, so it ranks first. In terms of growth factors, the countries in the forefront are Spain, Japan, Australia and Italy. As an emerging country in the photovoltaic industry, Japan is developing rapidly, both in the upstream polysilicon production, in the midstream solar cell production and downstream PV installation. Capacity has developed rapidly. In 2013, the installed capacity of photovoltaic cells in Japan was 6GW, which was 200% higher than that of 2GW in 2012, and the growth rate was amazing. This is closely related to the strengthening of Japan's national strength and the government's policy support. From the perspective of demand factors, the top ranked countries are Germany, the United States, China, Italy, and Japan. In 2013, the installed capacity of Germany and the United States reached 4GW and 3.5GW respectively. China's new installed capacity reached 10GW, an increase of 122% year-on-year, ranking first in the world. From the perspective of support capacity factors, the top ranked countries are Korea, Japan, the United States, and Germany. They have superior solar natural resources, strong financial strength, and advanced technical support to provide financial and technical support for photovoltaic production.

From the perspective of comprehensive factors, China, the United States, Germany, and Japan are ranked top, with the necessary technology, capital, policy, and environmental support for photovoltaic production, and are highly competitive in the global PV industry chain.

1.3 Cluster Analysis

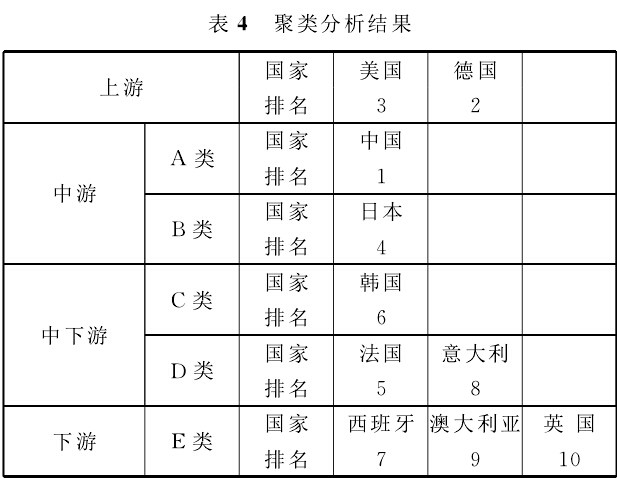

Using the industry chain factor scores obtained by factor analysis as a variable, cluster analysis of the competitiveness level of each country's industrial chain. The inter-group average connection method using systematic clustering method is based on the squared Euclidean distance, and the analysis results are relatively stable. The clustering results of the competitiveness level of each country's industrial chain are shown in Table 4.

From the results of factor analysis and cluster analysis, driven by the development of the international photovoltaic market and the domestic PV policy, China's photovoltaic industry has developed rapidly, both in terms of monocrystalline silicon production and battery and component production scale. The photovoltaic manufacturing country is advancing, and it is close to or leading the international level in technology, and the industrial chain is highly competitive. However, while the total scale of the photovoltaic industry has been greatly improved, due to various factors such as technology, capital, and policies, there are still differences between the various links of the industrial chain, between the upstream and downstream, and between the production capacity and the infrastructure. Balance. It is still in the midstream manufacturing industry with low technical content in the industrial chain.

2 Global and China's photovoltaic industry competitiveness dynamic analysis and path selection 2.1 Global PV industry competitiveness trends

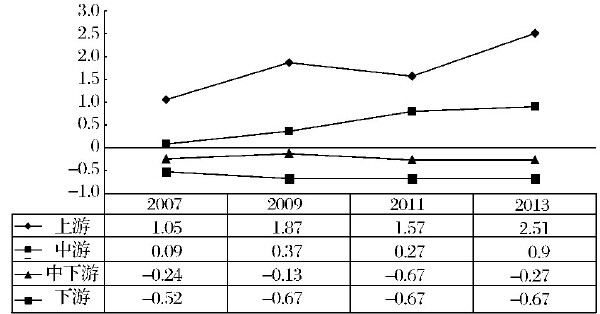

Based on the clustering results established above, the current trends in the competitiveness of countries in the global industrial chain are analyzed. According to the principal component analysis principle, the eigenvalue and eigenvector are calculated by the correlation coefficient matrix. The cumulative variance contribution rate of the first two principal components reaches 85.844%, which can represent most of the original data, so the two components are extracted. And analysis, calculate the principal component comprehensive score, the results are shown in Figure 1.

Figure 1 Trends in global PV industry chain competitiveness from 2007 to 2013

Can be seen from Figure 1. From 2007 to 2013, there are three trends in the development of the global PV industry chain: 1 The upstream industrial chain is in a state of rising volatility.

2 The midstream industry chain has shown a rising trend.

3 The middle, lower reaches and downstream industrial chains showed a steady rise.

The upstream industry chain has strong technical requirements, large capital investment, high requirements for enterprises, high entry threshold and strongest competitiveness. The mid-stream industrial chain mainly produces solar cells and photovoltaic modules, mostly labor-intensive industries, and does not require technical requirements for enterprises. High, the competitiveness is relatively weak; the downstream industrial chain mainly carries out the installation and application of photovoltaic systems, and the output is large, but the application level is not high and the competitiveness is weak. In short, the competitiveness and distribution of the PV industry chain are related to national policies, economic and technological development levels and its external environment. To achieve better development, a good external environment and strong corporate strength are needed.

2.2 China's photovoltaic industry path selection

Using the same method, calculate the ranking of the competitiveness of the photovoltaic industry in the ten countries from 2007 to 2013, as shown in Table 5.

Based on the current development status of the photovoltaic industry in the ten countries, and to enhance the international competitiveness of China's photovoltaic industry, efforts should be made from the following aspects: the government subsidizes “the right medicineâ€, increases the subsidies of the upstream high-risk photovoltaic manufacturing industry, and appropriately reduces the low-risk downstream photovoltaic power generation application link subsidies; Promote upstream production technology innovation, reduce dependence on foreign markets; improve solar cell solar cell conversion efficiency, enhance independent research and development capabilities; improve mid-stream component production quality, increase product added value; open downstream PV product application market, narrow supply and demand gap at each end of the industry chain To enhance the scale of industrial scale development and enhance the international scale competitive advantage of the photovoltaic industry.

3 Conclusion

China's photovoltaic industry development started late, the industrial base is weak, the efficiency and quality level of solar cells and components are still generally lower than the world's advanced level. The research and development of high-purity silicon production technology and the production of new high-efficiency solar cells are also lagging behind developed countries such as Europe and America. The photovoltaic industry still relies mainly on market-driven rather than technology-driven and lacks strong economic competitiveness. Although China's photovoltaic industry has a large production capacity, it has not been effectively digested by the domestic market. Although China has a high market share in the international market, it is only a huge number. From the perspective of quality, its competitiveness is weak. The explosive development of China's photovoltaic industry in the past few years is largely influenced by the policy subsidies of European and American countries. In 2012, the “double-issue†outbreak in Europe brought a huge blow to China's photovoltaic industry, which shows that China's photovoltaic industry is developing very much. To a certain extent, it depends on the international market and its industrial competitiveness is weak. Chinese enterprises are mainly concentrated in midstream enterprises, with relatively few upstream and downstream. Therefore, it is necessary to increase industrial adjustment and form a comprehensive industrial chain to have a more competitive advantage in the market. Focus on the development of clean, efficient, low-cost, new high-purity silicon and solar cell production technology, support technology-leading enterprises to expand production capacity, improve conversion efficiency, reduce production costs, and gradually promote the development of China's photovoltaic industry to the level of specialization and industrialization. Adjust the direction of government support and promote the sustainable and healthy development of the photovoltaic industry.

Cinnamon has a very long, interesting background; in fact, many people consider it one of the longest-existing spices in human history. The cinnamon leaf oil is yellow in color and is available in woody and spicy aroma which is extracted through steam distillation process.

The cinnamon is used in a few different ways to produce medicinally beneficial products.

Cinnamon Essential Oil,Natural Cinnamon Essential Oil,Pure Cinnamon Essential Oil,Organic Cinnamon Essential Oil

Xinhui Gangzhou Flavors&Fragrance Co.,Ltd , https://www.xhgzff.com